Engaging the Monopolisation of Global Tech Markets

Introduction

The COVID-19 pandemic has underscored the importance of internet access that is affordable, competitive, and widely available for workers, families, and businesses. However, the digital economy has become highly concentrated and prone to monopolization. Tech Giants, Amazon, Apple, Facebook, and Google—have come to play an important role in our economy and society and represent the underlying infrastructure for national and international exchanges of communications, information, and goods and services. As of September 2020, the combined valuation of these platforms is more than $5 trillion—more than a third of the value of the S&P 100. Thus, as we continue to shift our work, commerce, and communications online, these firms stand to become even more interwoven into the fabric of our economy and our lives; having captured control over key channels of distribution and functioning as gatekeepers. Just a decade into the future, 30% of the world’s gross economic output may lie with these firms and just a handful of others. It has diminished consumer choice, eroded innovation and entrepreneurship in the U.S. economy, weakened the vibrancy of the free and diverse press, and undermined Americans’ privacy.

Apple

Apple has significant and durable market power in the mobile operating system market. Apple’s dominance in this market involves its control on the iOS mobile operating system that runs on Apple mobile devices. This in turn has resulted in Apple’s monopoly power in the mobile app store market, controlling access to more than 100 million iPhones and iPads in the U.S. Apple’s mobile ecosystem has produced significant benefits to app developers and consumers.

Launched in 2008, the App Store revolutionized software distribution on mobile devices, reducing barriers to entry for app developers and increasing the choices available to consumers. Despite this, Apple leverages its control of iOS and the App Store to create and enforce barriers to competition and discriminate against and exclude rivals while preferencing its offerings. Apple also uses its power to exploit app developers through misappropriation of competitively sensitive information and to charge app developers supra-competitive prices within the App Store. Apple has maintained its dominance due to the presence of network effects, high barriers to entry, and high switching costs in the mobile operating system market. Apple is primarily a hardware company that derives most of its revenue from sales of devices and accessories. However, as the market for products like the iPhone has matured, Apple has pivoted to rely increasingly on sales of its applications and services, as well as collecting commissions and fees in the App Store. In the absence of competition, Apple’s monopoly power over software distribution to iOS devices has resulted in harm to competitors and competition, reducing quality and innovation among app developers, and increasing prices and reducing choices for consumers.

Amazon

Amazon has significant and durable market power in online retail markets. Although Amazon is frequently described as controlling about 40% of U.S. online retail sales, this market share is likely understated, and estimates of about 50% or higher are more credible. As the dominant marketplace in countries such as the United States and the United Kingdom for online shopping, Amazon’s market power is at its height in its dealings with third-party sellers. The platform has monopoly power over many small- and medium-sized businesses that do not have a viable alternative to Amazon for reaching online consumers. Thus, although Amazon has 2.3 million active third-party sellers on its marketplace worldwide, recent surveys estimate that about 37% of them—about 850,000 sellers—rely on Amazon as their sole source of income.

Amazon achieved its current dominant position, in part, through acquiring its competitors, including Diapers.com and Zappos. It has also acquired companies that operate in adjacent markets, adding customer data to its stockpile and further shoring up its competitive moats. This strategy has entrenched and expanded Amazon’s market power in e-commerce, as well as in other markets. The company’s control over and reach across its many business lines enables it to self-preference and disadvantage competitors in ways that undermine free and fair competition. As a result of Amazon’s dominance, other businesses are dependent on Amazon for their success and their survival.

Google has a monopoly in the markets for general online searches and advertising. Google’s dominance is protected by high entry barriers, including its click-and-query data and the extensive default positions that Google has obtained across most of the world’s devices and browsers as no alternate search engine serves as a substitute. Google maintained its monopoly over general search through a series of anticompetitive tactics. These include an aggressive campaign to undermine vertical search providers, which Google viewed as a significant threat. Over the years, Google has used its search monopoly to misappropriate content from third parties and to boost Google’s inferior vertical offerings while imposing search penalties to demote third-party vertical providers. Google has steadily proliferated its search results page with ads and with Google’s content, while also blurring the distinction between paid ads and organic results. As a result of these tactics, Google appears to be siphoning off traffic from the rest of the web, while entities seeking to reach users must pay Google steadily increasing sums for ads. Numerous market participants analogized Google to a gatekeeper that is extorting users for access to its critical distribution channel, even as its search page shows users less relevant results.

A second way Google has maintained its monopoly over general search has been through a series of anticompetitive contracts. After purchasing the Android operating system in 2005, Google used contractual restrictions and exclusivity provisions to extend Google’s search monopoly from desktop to mobile. Documents show that Google required smartphone manufacturers to pre-install and give default status to Google’s apps, impeding competitors in search as well as in other apps. Today, Google is ubiquitous across the digital economy, serving as the infrastructure for core products and services online. Through Chrome, Google now owns the world’s most popular browser—a critical gateway to the internet that it has used to both protect and promote its other lines of business. Through Google Maps, Google now captures over 80% of the market for navigation mapping services—a key input over which Google consolidated control through an anti-competitive acquisition and which it now leverages to advance its position in search and advertising. And through Google Cloud, Google has another core platform in which it is now heavily investing through acquisitions, positioning itself to dominate the “Internet of Things,” the next wave of surveillance technologies. In certain instances, Google has covertly set up programs to more closely track potential and actual competitors, including through projects such as Android Lockbox. As each of its services provides Google with a trove of user data, reinforcing its dominance across markets and driving greater monetization through online ads, Google increasingly functions as an ecosystem of interlocking monopolies by linking these services together.

Facebook has monopoly power in the market for social networking which is firmly entrenched and unlikely to be eroded by competitive pressure from new entrants or existing firms. In 2012, the company described its network effects as a “flywheel” in an internal presentation prepared for Facebook at the direction of its Chief Financial Officer. This presentation also said that Facebook’s network effects get “stronger every day.” Documents produced during the US investigation into Facebook show that it has tipped the social networking market toward a monopoly, and now considers competition within its own family of products to be more considerable than competition from any other firm. Facebook has also maintained its monopoly through a series of anticompetitive business practices. The company used its data advantage to create superior market intelligence to identify nascent competitive threats and then acquire, copy, or kill these firms. Once dominant, Facebook selectively enforced its platform policies based on whether it perceived other companies as competitive threats. In doing so, it advantaged its services while weakening other firms.

Furthermore, the commercial and economic dominance of tech giants has attracted the attention of the powerful Chinese state and the supranational state entity of the EU. The dominance of tech giants has provoked responses from powerful entities to curtail some activities of these tech giants/titans. Some of these tech giant companies were fined for unfair practices in the EU while others were cited for privacy concerns. Some tech giants/titans were also accused by the EU and other stakeholders of hoarding IT human resources talents within a closed circle or restricting the mobility of these individuals through tacit agreements. Thus, internationally, there has been a marked rise in the anti-monopoly and antitrust instincts which advocates monopolies and titans if they are proven to practise unfair competition. This was recently shown in a US Pew Report.

At the individual firm level, the Big Five’s market shares have risen sharply (Figure 2.). In 2019, their market shares are substantially large, particularly in the case of Apple, which generates nearly the 75% of its industry sales. These data indicate that the industries analysed resemble more oligopolies than competitive markets.

Another commonly used measure to assess firms’ market power is markups, computed as the ratio between prices and marginal costs. In an ideal perfectly competitive market, where firms are price takers, prices are equal to marginal costs and therefore markups are equal to one. Clearly, the perfectly competitive market of classical economics is more an abstraction than a reality, but still, markups are valid indicators to grasp the market power of large corporations. In the industries where Amazon and Apple operate, markups have remained relatively stable throughout the period considered, while they have eventually declined in Microsoft’s. On the contrary, in the case of Alphabet’s industry, we observe an initial increase in markups and then a relatively stable behaviour. The most surprising case is perhaps Facebook, where the relative change in markups reached a peak of more than 800% in 2017 after a continuous rise. Not surprisingly, given their relative weight, the trends in mark-ups for the Big Five corporations reflect an industry-wide one.

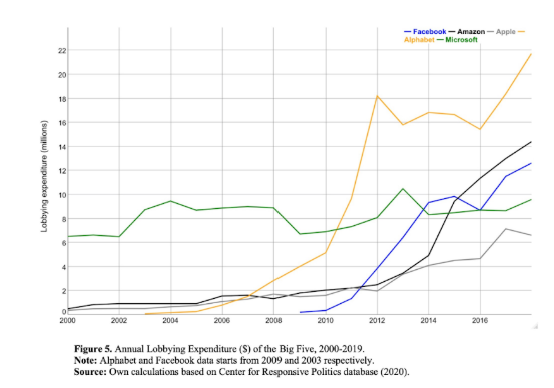

Beyond purely economic criteria, another light under which evaluating giant tech firms operating is political. Studies that chart lobbying expenditure can be used as a proxy to capture this additional dimension. As Tech Giants are shown to spend whooping capitals in lobbying, ranging from $6 to $22 million in 2018, placing all of them in the US top 1% of the lobbying expenditure distribution, this highlights how large corporations are not only economic but also political agents, thereby making it difficult to separate the political and the economic sphere when discussing their activities. Take Facebook and Google together. These two firms hold more private information about the world’s population than any other entities on earth. They also, collectively, have an apparent power to influence elections; perhaps not to decide them, but enough to swing a close vote. Should that power come into the hands of an entity determined to stay in office forever, the consequences could be truly alarming. It may begin, innocuously enough, with the idea that tech is doing its national duty as it aids the state. But it is apparent, based on the history of monopoly in the last century, that this is indeed the road to serfdom

Two Main Understandings of Tech Monopolisation

Antitrust, Market Operations and Monopoly Power

‘Imagine a place where trespassers leave no footprints, where goods can be stolen an infinite number of times and yet remain in the possession of their original owners, where businesses you never heard of can own the history of your personal affairs, where only children feel completely at home, where the physics is that of thought rather than things, and where everyone is as virtual as the shadows in Plato’s cave.’ Barlow. J EFF Co-founder.

Our earliest conceptions of the digital economy and its technological markets # suggested that in cyberspace, there could be no such thing as a lasting monopoly. The Internet would never stand for it. Business models and corporate operations were now moving at Internet speed: a three-year-old firm was middle-aged; a five-year-old firm was almost certainly near death. ‘Barriers to entry’ was a twentieth-century concept. Now, competition was always just ‘one click away’.

But after a decade of open chaos and easy market entry, something surprising did happen. As the 2010s began, a few firms – Google, Facebook and Amazon – did not disappear. They hit that five-year mark of obsolescence with no signs of impending collapse or retirement. Instead, the major firms seemed to be sticking, and even growing in their dominance. Suddenly, there weren’t a dozen search engines, each with a different idea, but a single search engine. There were no longer hundreds of stores that everyone went to, but one ‘everything store’. And to avoid Facebook was to make yourself a digital hermit. There stopped being a next new thing, or at least, a new thing that was a serious challenge to the old thing. In this way, the tech industry became largely composed of just a few giant trusts: Google for search and related industries, Facebook for social media, and, in the United States, Amazon for online commerce. While competitors remained in the wings, their positions became marginalized with every passing day. This RR will illustrate three ways tech monopolies consolidated their power.

Buying

Tech Giants have been known to acquire and buy out firms that represent competition. Together, the 4 Tech Giants have acquired hundreds of companies just in the last ten years. In some cases, these dominant firms acquired nascent or potential competitors to neutralize a competitive threat or to maintain and expand the firm’s dominance. In other cases, a dominant firm acquired smaller companies to shut them down or discontinue underlying products entirely—transactions aptly described as “killer acquisitions. An example of this was when Facebook bought out the up-and-coming Instagram. As Time Magazine came to put it, ‘Facebook buying Instagram conveyed to investors that the company was serious about dominating the mobile ecosystem while also neutralizing a nascent competitor.’ This highlighted a gap within antimonopoly laws as both American and European regulators found themselves unable to find anything wrong with the takeover. The American analysis remains secret while the United Kingdom’s report reached the extraordinary conclusion that Facebook and Instagram were not competitors predicated on a) Instagram was a photo-taking app, meaning that Facebook was not competing with Instagram for consumers b) Instagram did not have advertising revenue, so it did not compete with Facebook in advertising either. In total, Facebook has managed to string together more than 90 unchallenged acquisitions, which seems impressive, until you consider that Google got away with at least 270.

Cloning

A further means through which tech monopolies might distort the competitive nature of the market is through cloning the services of their competition and taking advantage of their monopolies of scale. Facing potential challenges from Yelp’s popular reviews of local businesses in the early 2010s, Google created its own local sites attached to Google Maps. And when google as a newcomer realised that The value in any such site would rest in the quality of its user reviews, It solved the problem by simply purloining Yelp’s reviews and putting them on its site, making Yelp essentially redundant, and also harvesting the proceeds of its many years of work. Facebook cloned so many of its rival Snapchat’s features that it began to seem like a running joke – most notably, its ‘stories’ feature. However, there is a line where copying and exclusion become anti-competitive, where the goal becomes the maintenance of monopoly as opposed to real improvement and innovation. When companies such as Facebook spy on competitors or summon a firm to a meeting just to figure out how to copy it more accurately or discourage funding of competitors, a line is crossed.

State Protectionism

A rising means of the proliferation of global tech markets is through nationalistic practices and protectionism. Beyond Anglo-American practices, China’s tech sector is, in particular, a by-product of state involvement and encouragement. However, it is relevant to note that China has a highly talented class of software engineers and scientists, an entrepreneurial culture, and a citizenry that has rapidly embraced new technologies. And it is also true that its tech sector has more competition than other parts of the Chinese economy. It stands to reason that China might only be a middling tech power if not for several types of state intervention. For one thing, most of the major American tech platforms are either blocked (Facebook, Twitter) or heavily disadvantaged (Google). That, along with extensive state subsidization – tech is regularly included in China’s ‘five-year plans’ – has fertilized the growth of domestic giants. These include China Mobile, the state-owned mobile operator; Tencent, the giant of social media, an equivalent to Facebook and Twitter; Alibaba, which is like a combination of eBay, Amazon and PayPal; Baidu, China’s leading search engine; and Huawei.

This in turn has led to Mark Zuckerberg of Facebook and other tech leaders offering a stark warning to those who might want more competition in the tech industries. It goes like this: ‘We understand that we’ve made mistakes. But don’t you realize that if we damage the current tech giants, we’ll just be handing over the future to China? Unlike us, the Chinese government is standing behind its tech firms, because it knows that competition is global, and it wants to win.’ (Wu, 2020) Some add that at least firms like Facebook and Google were founded in places with progressive ideals and democratic values. A future dominated by China would be far worse for the individual rights that we value. This is Big Tech’s version of the ‘too big to fail argument. Its appeal is superficial and nationalistic. It may also appeal to some who believe in an ‘us versus them’ populist narrative or become through its assent, a self-fulfilling prophecy.

Competition is a critical source of innovation, business dynamism, entrepreneurship, and the “launching of new industries.” Vigorously contested markets have been and always will be a critical competitive asset. While large firms with significant resources may invest in research and development for new products and services, competition forces companies to “run faster” to offer improved products and services. Without competitive pressure, some level of innovation may still occur, but at a slower, iterative pace In recent decades, however, there has been a sharp decline in new business formation as well as early-stage startup funding. The number of new technology firms in the digital economy has declined, while the entrepreneurship rate—the share of startups and young firms in the industry as a whole—has also fallen significantly in this market.171 Unsurprisingly, there has also been a sharp reduction in early-stage funding for technology startups. The rates of entrepreneurship and job creation have also declined over this period. The entrepreneurship rate—defined as the “share of startups and young firms” in the industry as a whole— fell from 60% in 1982 to a low of 38% in 2011.

Techno-colonisation; tech giants in developing countries

Today, a new form of corporate colonisation is taking place. Instead of the conquest of land, Big Tech corporations are colonising digital technology. The following functions are all dominated by a handful of US multinationals: search engines (Google); web browsers (Google Chrome); smartphone and tablet operating systems (Google Android, Apple iOS); desktop and laptop operating systems (Microsoft Windows); office software (Microsoft Office, Google G Suite); cloud infrastructure and services (Amazon, Microsoft, Google, IBM); social networking platforms (Facebook, Twitter); transportation (Uber, Lyft); business networking (Microsoft LinkedIn); streaming video (Google YouTube, Netflix, Hulu); and online advertising (Google, Facebook) – among others. GAFAM now comprise the five wealthiest corporations in the world, with a combined market cap exceeding $3 trillion.9 If South Africans integrate Big Tech products into their society, the United States will obtain enormous power over their economy and create technological dependencies that will lead to perpetual resource extraction. Early research and case examples suggest the economic impact of Big Tech intermediaries is detrimental to local African industries. Murphy, Carmody and Surborg, who studied the role of ICTs among small, medium, and micro-sized enterprises (SMMEs) in South Africa’s and Tanzania’s wood and tourism industries, found that ICTs introduced the dominance of information intermediaries. Increased use of ICTs also led to greater worker surveillance in some instances. They concluded that ICT integration is, on balance, benefiting foreign-owned businesses and corporations.

Facebook’s Free Basics service offers another case of how Big Tech corporations expand their empire in the Global South. Despite initially dismissing claims of an underlying profit motive, Free Basics was always a way to promote Facebook to first-time Internet users, grow its user base, and provide a competitive advantage to the corporation in emerging markets. Free Basics offers a stripped-down version of free Internet services to people with little or no disposable income. Facebook decides which content and websites the poor can access – while conveniently providing Facebook itself within the app. Free Basics is zero-rated by ISPs, meaning that data transfers inside the app are paid for by ISPs instead of their customers. The ISPs hope that the limited Internet experience will lead to paying customers who, having tasted a free sample, will purchase data for the full experience.

In May 2010, 50 mobile operators launched it in 45 countries, including DRC, Rwanda, Uganda, and Ivory Coast. Facebook hoped to access emerging markets with low Internet penetration rates and high data costs but with high mobile phone uptake and tremendous demographic growth. By targeting these users, Facebook Zero sought to make Facebook their first entry point to the web, while boosting its user growth ahead of its 2012 initial public offering (IPO). That same year, Twitter, Wikipedia, and Google launched similar zero-rated services invariably presented as efforts targeting the ‘next billion users’ in emerging, mobile-first markets. Foreign corporations undermine local development, dominate the market, and extract revenue from the Global South, with power obtained primarily through the structural domination of digital architecture, which leads to more general forms of imperial control. Thus, Free Basics resulted not only in Facebook playing Internet gatekeeper of the poor, it also violates net neutrality laws: zero-rated offerings place content providers on an unequal footing. Several countries have terminated Free Basics, in part due to popular backlash. However, Internet.org has put over 100 million users from over sixty countries, including South Africa, into the Facebook platform, which channels them towards the Facebook ecosystem. Integrating platforms like Facebook outside the US does more than drain local advertising revenue: it undermines various forms of local governance. Seventy-five per cent of web publisher’s traffic now comes from Google (46 per cent) and Facebook (29 per cent).39 Centralisation of services into their hands provides them with centralised control over communications – by way of code. These two firms filter search results and news feeds with proprietary black box algorithms, granting them enormous power to shape who sees what news. Leftist outlets have published data suggesting that Google censors socialist views, while Facebook has been found to favour mainstream liberal media.

This illustrates two broader and interrelated trends in the digital industry when expanding, digital experiments on marginalized populations and data extraction. There is increasing evidence that vulnerable and disadvantaged populations, such as minority groups, refugees, and impoverished communities are prime, albeit largely nonconsenting subjects of digital experiments – be they designed to ‘help’ or surveil these communities. Data extraction, for its part, is central to the digital economy. It is key to building unique, rich datasets that train competitive algorithms, which are then generally used to connect businesses to customers.

The story of the tech industries should not just be a story of the United States and China. Yet except for a handful of other countries, including Israel, Japan, Taiwan and the Scandinavian nations, very few countries have successfully developed domestic tech industries of real significance. It is unusual for the world to be ruled not just by domestic monopolies, but fully global monopolies. The question for the rest of the world is, does all comparative advantage lie with only two countries? Over the next decade, if wealth is to be more evenly distributed, how can it do so if certain companies based out of specific countries enjoy asymmetrically dependent relationships, threatening to ‘eat everything’?

Rationalising Potential Approaches

Broadly speaking, it is possible to classify regulators’ preferences for antitrust and competition policy into two macro-categories: firm-based and market-based. Such ideal categories of preferences are not fixed and can switch over time. The firm-based approach, which derives from the so-called Chicago tradition, does not see industry concentration as a problem per se, as long as consumers’ welfare is not harmed. Building on this tradition, it follows that policymakers’ intervention should be guided more by changes in markups rather than concentration indexes. The reason stems directly from one of the milestones of economics: The First Welfare Theorem. Since society’s welfare is maximised in a world of price-taking firms, earning zero profits, the higher the markups the further we are from the Pareto optimum, whereby the lower is consumers’ welfare.

On the other hand, the market-based approach, also called Ordoliberal, is concerned in maintaining free and competitive markets, ideally populated by a few very large firms and by many small-medium enterprises, thereby enhancing the principles of economic freedom. It follows logically that under these preferences high industry concentration and large market shares are reasons to intervene. Arguably, these different approaches constitute the Atlantic divide existing between American and European policymakers: the former pursuing the firm-based approach, whereas the latter the market-based one. The American firm-based approach can be reflected in the more lenient orientation of US regulators towards big businesses and the laxer blocking of dominance mergers concerning European counterparts (Kwoka and White 2008, Bergman et al. 2010). Indeed, during the Bush administration American antitrust law was relaxed and the Department of Justice changed its guidelines to make it more difficult to sue large corporations for anti-competitive actions (Cassidy 2013). Instead, the market-oriented approach of European authorities can be found in the more aggressive antitrust policies against large tech companies, exemplified by the Google Shopping decision of the European Commission, wherein Google was fined for its abuse of dominance (Portuese 2020).

Thus, three main suggestions have been individuated for policymakers on both sides of the Atlantic. The first is not to focus on concentration per se but to evaluate it within a broad set of indicators and factors, such as the creation of barriers preventing the entry of new competitors and the actual impact on consumers. Furthermore, lower competition, to some extent, can be tolerated if it is the result of superior products, and if it can foster innovation (Aghion and Howitt 1992). Secondly, there is the need to build transnational cooperation among regulators, as suggested by Büthe (2015). The rationale behind this argument is that these companies are acquiring an ever-increasing global dimension, the domestic regulator, even when its jurisdictional reach is large –as in the case of the US and Europe – and this may prove inadequate in a democratic context. Moreover, increasing cooperation between national regulators may result in a more homogenous enforcement of competition and antitrust policy, which is lacking at the moment. Finally, large corporations should be evaluated not only for their economic but also political weight. The goal of regulators and policymakers, in this respect, should be minimising the preferential access to the politics of tech giants given by their superior financial resources.

QARMA

What are the potential spillover effects of Big Tech regulation and how would ECOSOC ensure countries with varying levels of development are equally insulated from such effects?

To what extent can a global framework that restores the Antimonopoly Goals of the Antitrust Laws be agreed upon?

How might member nations collaborate to allow capacity building for data-driven digitalisation and policymaking about tech markets?

What level of collaboration is required between public and private sectors in regulating global tech markets and how would countries ensure that multinational companies are held to the same standards internationally?

How would countries collaborate to continue identifying, classifying and overcoming the dangers of social media within an ever-mercurial digital landscape?